GoldTent Oasis is dedicated to our friend and founder John F. Murphy (Wanka) of Key West, Florida without whom this website would not exist. Gone but never forgotten.

ENTER ~ Post by the Golden Rule. Gentlemanly conduct is the attire of the day. GoldTent Oasis is not responsible for content or accuracy of posts DYODD. ~~~~~~~

It’s not only Chinese tourists, business travelers, and property buyers who’re not showing up, but also travelers from all over the world who’ve gotten second thoughts about sitting on a plane (VIDEO=10 minutes).

I owned TRX in the past and have followed it over the years. And a whole lot of years it’s been! I appreciate Jim Sinclair’s contributions to our cause but building his mine is taking forever.

I guess there is always some companies pulling ahead and others going down. Would be nice to know such things ahead of time. 🙂 I don’t feel that MUX is going down for the count. It’ll be back at some point. If it wasn’t for Skeena I’d really be sucking hind ti*!

R640 – yeah, panic selling? I think not. Probably something more like the complimentary up 100 DOW pts. pre-market tomorrow to start the day as is the norm. Maybe more.

Ipso – Do you own any TRX? I haven’t owned it in quite some time. Some of the shares I used to do OK with have really performed poorly in the last several years, AAU, GPL, course MUX. Several others. Doesn’t look like TRX has fared much better.

Maybe this is the new era where Wallbridge, Skeena, Gatling, etc. are the new high flyers?

Welcome to edition 504 of Insider Weekends. Insider buying decreased last week with insiders purchasing $100.09 million of stock compared to $177.87 million in the week prior. Selling also decreased with insiders selling $1.22 billion of stock last week compared to $5.4 million in the week prior. The prior week’s numbers included the huge $4.06 billion sale of Amazon.com (AMZN) by Jeff Bezos.

Sell/Buy Ratio: The insider Sell/Buy ratio is calculated by dividing the total insider sales in a given week by total insider purchases that week. The adjusted ratio for last week dropped to 12.16. In other words, insiders sold almost more than 12 times as much stock as they purchased. The Sell/Buy ratio this week compares unfavorably with the prior week, when the ratio stood at 30.37.

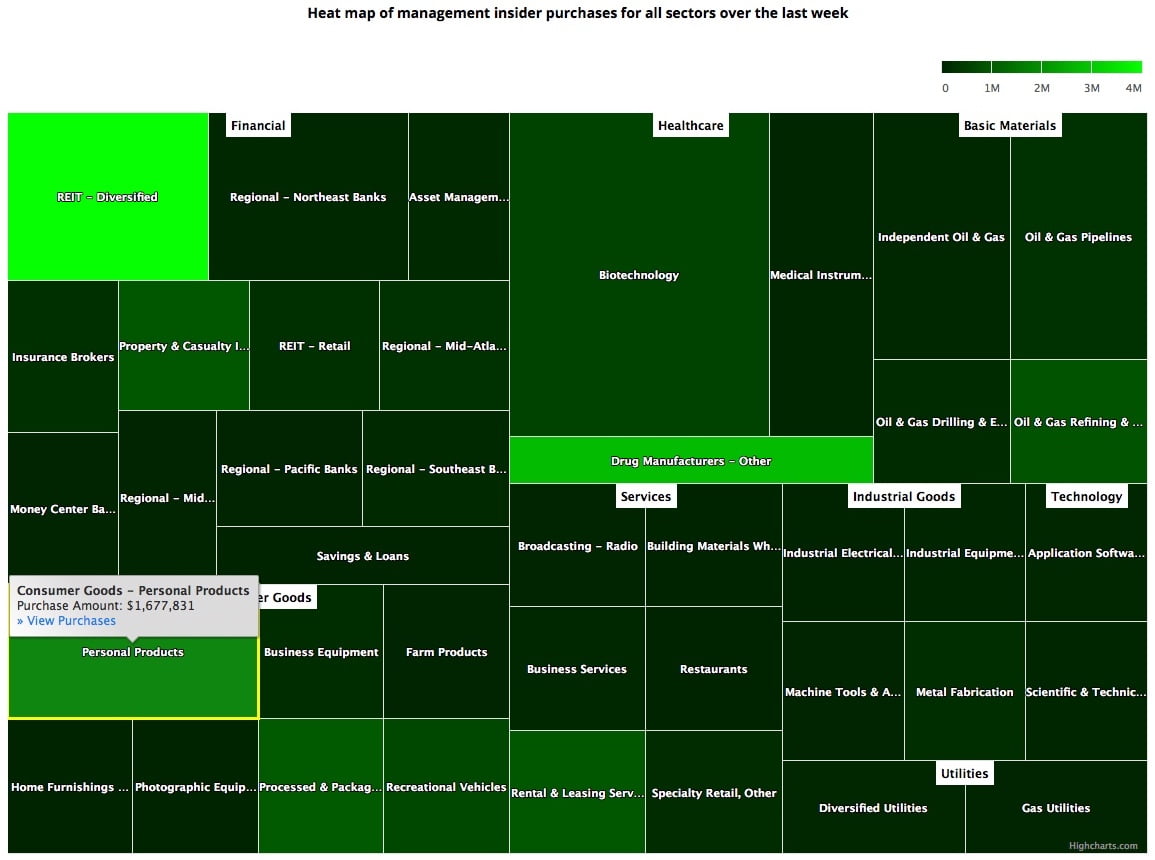

Insider Sector Heat Map February 14, 2020 (click to enlarge)

MaNote: As mentioned in the first post in this series, certain industries have their preferred metrics such as same store sales for retailers, funds from operations (FFO) for REITs and revenue per available room (RevPAR) for hotels that provide a better basis for comparison than simple valuation metrics. However metrics like Price/Earnings, Price/Sales and Enterprise Value/EBITDA included below should provide a good starting point for analyzing the majority of stocks.

Tanzanian Gold announces 4,291,000 ounces of gold contained in unclassified resources at the conclusion of its Phases 1 & 2 Resource Upgrade drilling along the 1.2km Buckreef Shear Zone

Have to agree with you though, Hitlery is her and Bloombugs worst nightmare. Together, they couldn’t win a Demonrat beauty pageant, much less an election.!! 🙂

But it’s the “perfect storm” still, right? I mean it’s always the “perfect storm” with Sprott. It was the “perfect storm” for gold to break $5000 in 2014, 2015, 2016, 2017, and 2018. Silver (especially those Panda coins they sell) is just about to go “parabolic” in the “perfect storm” because… well, you know… fiat and the fed and all that. Just wanted to make sure it’s still the “perfect storm”

Anywho… it’s the “perfect storm” y’all… and Sprott is selling bullion as fast as they can… cause it’s about to skyrocket any minute now. So they are selling… good deals too.

There is a weekly of silver, the low was 2016( these things take time, so do not get in a hurry).

late 15, early 16 low, then 1-2-3-4-5, to 1 Up to July 2016 which is 1 of 1. Then an ABC into Nov 2018, low, That was 2 of 1.

We are working on 4 of 1, or starting 5 of 1 which should go above wave 1.

So this year we should see 21-22 silver, then wave 2 of 3 of 1( maybe 3 months pull back).

I would expect 2021 to be spent above 20.

Wave 2 took 2 years, Wave 3 should top in 2023 at or above 50.

How is that for you?

Look we had a bull in silver from 2000-2011, same with gold.

Gold led the first one, and pre-2007, gold was up way more than silver.

Now we have had a 10 year bear, and we are getting ready for the next one.

In this one silver leads, but even bull markets in PM’s has a ton of volatility, so protect yourselves.

Pull some Fib’s on silver from 2011 high’s will give you a road may and where the rest stops are at.

Equities at record prices garner all the attention. Yet the manic behavior in global bond markets is more extraordinary and consequential. U.S. fixed income ETFs attracted another $7.3bn this week (ETF.com), as “money” keeps rolling in. The $64 TN question is how much speculative leverage continues to accumulate throughout global bond and derivatives markets. Here again, the timing of the coronavirus outbreak is of great consequence – inciting speculative excess and attendant leverage when global fixed-income was already engulfed by powerful Inflationary Biases. Added leveraging works to inject additional liquidity into already over-liquefied global markets. And the last thing overheated global risk markets – with such powerful Inflationary Biases – needed at this point was additional liquidity.

I view the equities Bubble as an offshoot of the greater Bubble that continues to inflate in global debt, securities Credit and derivatives markets. On the one hand, it is extraordinary to see equities markets essentially dismiss such consequential developments in China. It does, however, present important support for the Bubble Thesis. Equities rallied to record highs just months before the LTCM/Russia collapse in 1998. Stocks rallied to record highs in 2007 even as the mortgage finance Bubble faltered.

It’s only fitting that global stocks rally to record highs as the faltering China Bubble places the global Bubble in serious jeopardy. If the coronavirus stabilizes over the coming weeks and months, attention can then shift to November U.S. elections. It’s poised to be One Extraordinary Year.

A Friday CNBC headline: “White House Considering Tax Incentive for More Americans to Buy Stocks, Sources Say.” A strong equities market boosts optimism for a Trump reelection – bullishness that spurs further stock gains. Yet there is potential for self-reinforcing dynamics to the downside. A break in stock prices would incite election nervousness and heightened market risk aversion. Can this game sustain for another nine months?

That equities can run higher in the face of mounting risks is not as confounding as it might first appear. Credit drives the global Bubble – and Credit in the near-term is further benefiting from the outbreak.

Overheated securities (speculative) Credit is really benefited.

Global monetary stimulus is further assured – rate cuts and more QE. One can now add aggressive PBOC liquidity injections to the Fed and global central bank QE throwing gas on a speculative fire raging throughout global fixed-income markets.

Beijing has declared a “people’s war” against the forces of Bubble deflation. And this explains why markets so confidently operate under the assumption a bust won’t be tolerated. Extraordinary fragilities only ensure epic stimulus; Chinese and global Punchbowls Runneth Over. “Washington will never allow a U.S. housing bust.” “The West will never allow Russia to collapse.” There are monumental presumptions that underpin historic boom and bust cycles. “The Beijing meritocracy has everything under control.”

Staring at a rapidly unfolding economic and financial crisis, Beijing has made the decision to move forward with efforts to get their faltering economy up and running. This comes with significant risk. Global markets, by now fully enamored with aggressive monetary and fiscal stimulus, are predisposed to fixate on potential reward (keen to disregard risk). That future students of this era will be more than a little confounded has been a long-standing theme of my contemporaneous weekly chronicle. Booming market optimism in the face of what has been unfolding in China will ensure years and even decades of head-scratching.

China is definitely not alone in gambling with aggressive late-cycle stimulus, as it desperately tries to postpone the unavoidable dreadful downside after historic Bubble Inflations. Coming at this key juncture of end-of-cycle fragilities, it’s a challenge to envisage more delicate timing for such an outbreak – in China and globally. Clearly, when global markets hear “stimulus” they immediately salivate over the thought of bubbling liquidity and ever higher securities prices. Critical nuances of global Inflation Dynamics go unappreciated.

as a Run Mate until he realizes How many have died getting in the way of her ambitions…..Its a DEATH wish…Its a BAD IDEA MIKE ! ya better rethink that one !

A Mike Bloomberg presidential ticket with Hillary Clinton as vice president would mean California-style gun control for everyone.

I wouldent sell you a Life Insurance Policy for NO amount of money ….